English

English Türkçe

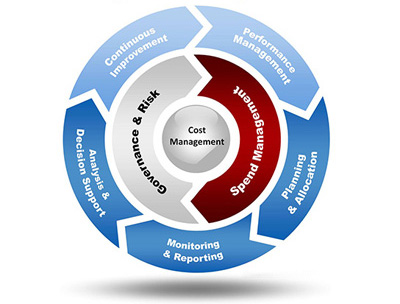

TürkçeCost Management

Cost accounting has long been used to help managers understand the costs of running a business. Modern cost accounting originated during the industrial revolution, when the complexities of running a large scale business led to the development of systems for recording and tracking costs to help business owners and managers make decisions.

In the early industrial age, most of the costs incurred by a business were what modern accountants call "variable costs" because they varied directly with the amount of production. Money was spent on labor, raw materials, power to run a factory, etc. in direct proportion to production. Managers could simply total the variable costs for a product and use this as a rough guide for decision-making processes.

Some costs tend to remain the same even during busy periods, unlike variable costs, which rise and fall with volume of work. Over time, the importance of these "fixed costs" has become more important to managers. Examples of fixed costs include the depreciation of plant and equipment, and the cost of departments such as maintenance, tooling, production control, purchasing, quality control, storage and handling, plant supervision and engineering. In the early twentieth century, these costs were of little importance to most businesses. However, in the twenty-first century, these costs are often more important than the variable cost of a product, and allocating them to a broad range of products can lead to bad decision making. Managers must understand fixed costs in order to make decisions about products and pricing.

Project Cost Management to be provided, includes management of phases through feasibility and bid process through execution, completion and operation stages.

In execution phase it is based on project planning and indicates the cost of activities after resource loading has performed. An effective cost management target is to complete the project within its budget. Cost plans shall be showing the status of project over its budget and warns about negative cash flows if there is any throughout the project. Regular reporting with performance indicators is essential.

IPMS can provide budget reviews and revisions on specified periods as per project's requirements and regular cost controlling with earned value management. Project management can be supported by cost performance indicators and future forecasts.

In the early industrial age, most of the costs incurred by a business were what modern accountants call "variable costs" because they varied directly with the amount of production. Money was spent on labor, raw materials, power to run a factory, etc. in direct proportion to production. Managers could simply total the variable costs for a product and use this as a rough guide for decision-making processes.

Some costs tend to remain the same even during busy periods, unlike variable costs, which rise and fall with volume of work. Over time, the importance of these "fixed costs" has become more important to managers. Examples of fixed costs include the depreciation of plant and equipment, and the cost of departments such as maintenance, tooling, production control, purchasing, quality control, storage and handling, plant supervision and engineering. In the early twentieth century, these costs were of little importance to most businesses. However, in the twenty-first century, these costs are often more important than the variable cost of a product, and allocating them to a broad range of products can lead to bad decision making. Managers must understand fixed costs in order to make decisions about products and pricing.

Project Cost Management to be provided, includes management of phases through feasibility and bid process through execution, completion and operation stages.

In execution phase it is based on project planning and indicates the cost of activities after resource loading has performed. An effective cost management target is to complete the project within its budget. Cost plans shall be showing the status of project over its budget and warns about negative cash flows if there is any throughout the project. Regular reporting with performance indicators is essential.

IPMS can provide budget reviews and revisions on specified periods as per project's requirements and regular cost controlling with earned value management. Project management can be supported by cost performance indicators and future forecasts.